Engineering the Logic Behind Deep Tech Deals

How to make scientific risk legible, translate evidence into leverage, and shape the negotiation before the term sheet arrives.

The strongest fundraisers in Deep Tech are shaped long before legal language appears, because the decisive work happens when scientific risk becomes legible, when ownership is framed with discipline, and when the room is designed before anyone sits down.

Deep Tech fundraising creates a particular kind of misunderstanding because founders often enter the conversation with years of scientific work behind them, and investors enter with portfolio math, internal timelines, and a mandate to allocate capital under uncertainty, which means that the room is filled with intelligence on both sides even as language, pacing, and decision criteria move on different tracks.

That mismatch explains why many strong companies weaken their own position before a term sheet ever appears, since they describe the science with rigor, they describe the market with hope, and they describe the financing with a degree of vagueness that allows the other side to define both the risk and the price. A founder who wants stronger outcomes needs a more deliberate frame, because deep tech negotiation begins when the company decides how evidence, ownership, and timing will be translated into investable reality.

In Deep Tech, negotiation functions as the operating system that connects science, capital, and execution, and the founder who understands that connection early gains clarity in valuation, credibility in the room, and resilience across the life of the company.

This guide sits within The Scenarionist’s broader work on Deep Tech Negotiation, where equity, market validation, valuation logic, BATNA, and negotiation design are examined with greater depth and practical continuity.

The full Deep Tech Negotiation Playbook series is available here through The Scenarionist Premium.

Unlock the full experience by becoming a Premium Member!

The Scenarionist Premium is built for founders, investors, and operators who want sharper frameworks, deeper analysis, and access to actionable insights across the Deep Tech landscape.

1. The Strange Gravity of Physical Systems

Deep tech companies carry a different economic rhythm, because atoms, factories, clinical pathways, energy systems, and supply chains impose their own tempo, and because intellectual property often carries university, governmental, or strategic constraints that require a wider view of the deal than a simple exchange of cash for shares. When this complexity is handled with precision, investors receive a coherent picture of how risk will be reduced over time, and founders preserve the strategic room that serious company building requires.

Three structural realities shape the discussion from the beginning.

The first is that the product in an early-stage round is ownership, which means the founder is offering access to a future company whose value depends on milestones that have not yet been reached.

The second is that proof arrives in forms that differ from conventional venture shorthand, because design partners, technical validation, letters of intent, patent position, scale-up feasibility, and readiness levels often matter more than near-term revenue.

The third is that the negotiation rarely belongs to two people alone, since co-founders, university offices, strategic partners, boards, internal investment committees, and future syndicate members can all influence the outcome even when they do not speak first.

This operating environment rewards founders who can move between technical depth and financial clarity without flattening either one, because the investor needs a business that can carry the science forward, and the company needs capital that fits the tempo of the underlying industrial journey.

2. Evidence Creates Leverage Long Before Valuation Does

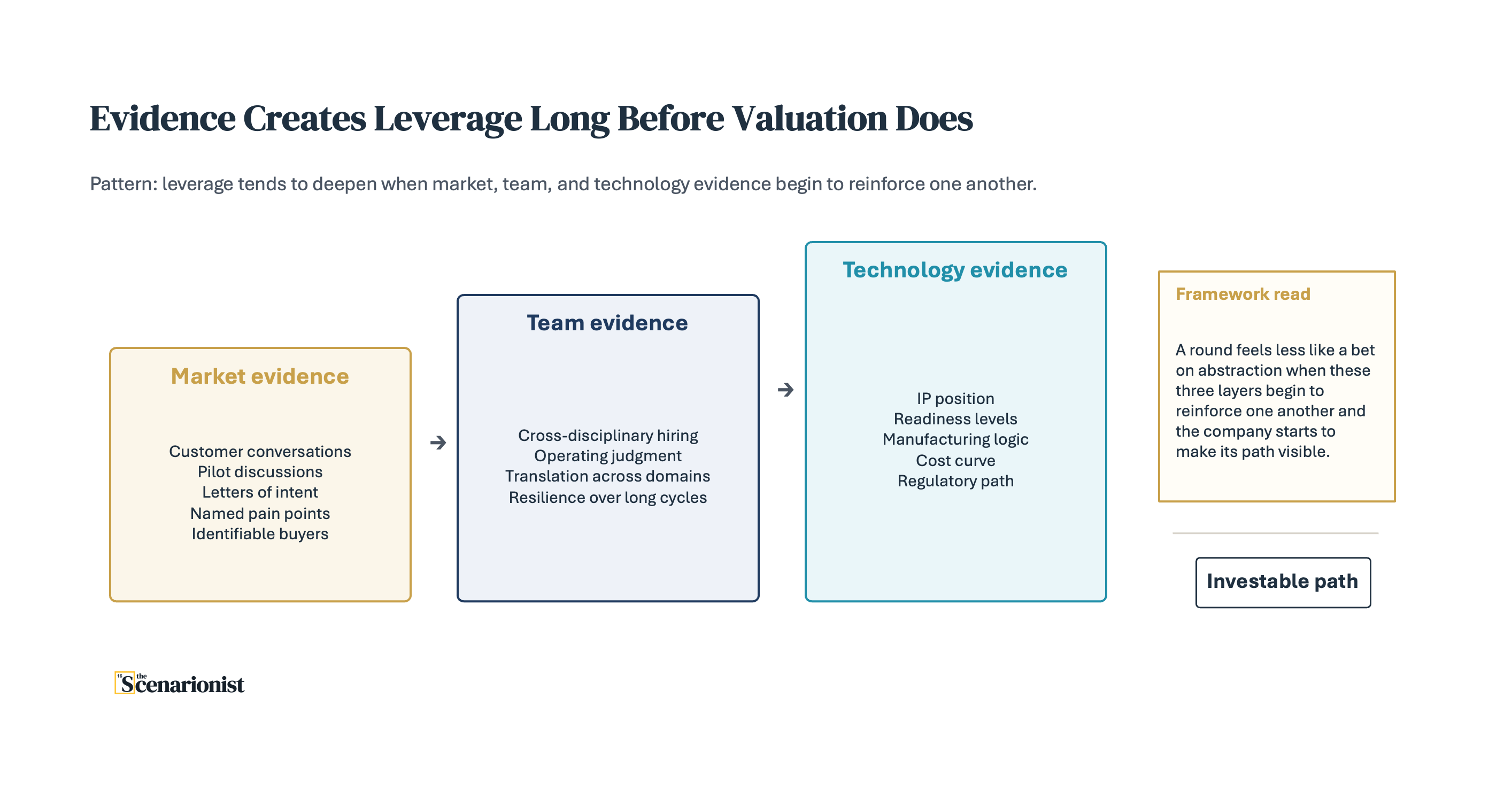

One useful way to think about leverage in deep tech is to begin with evidence first, because valuation conversations usually become more coherent after the company has shown why the problem is real, why the team is credible, and why the technology can travel from laboratory promise toward commercial relevance.

Market evidence often begins with customer conversations, pilot discussions, or letters of intent, all of which help the founder move the conversation away from broad possibility and toward named pain points, identifiable buyers, and visible demand.

Team evidence follows a similar logic, since investors are often trying to understand whether the company can recruit across disciplines, translate technical insight into operating decisions, and remain resilient over a development cycle that may prove longer than anyone initially hoped.

Technology evidence then adds another layer, because intellectual property, readiness levels, manufacturing logic, cost curves, and regulatory pathways help technical progress feel investable in business terms.

When these three layers begin to reinforce one another, a round tends to feel increasingly coherent, and the investment starts to look like a structured commitment to a company that has begun to make its path visible.

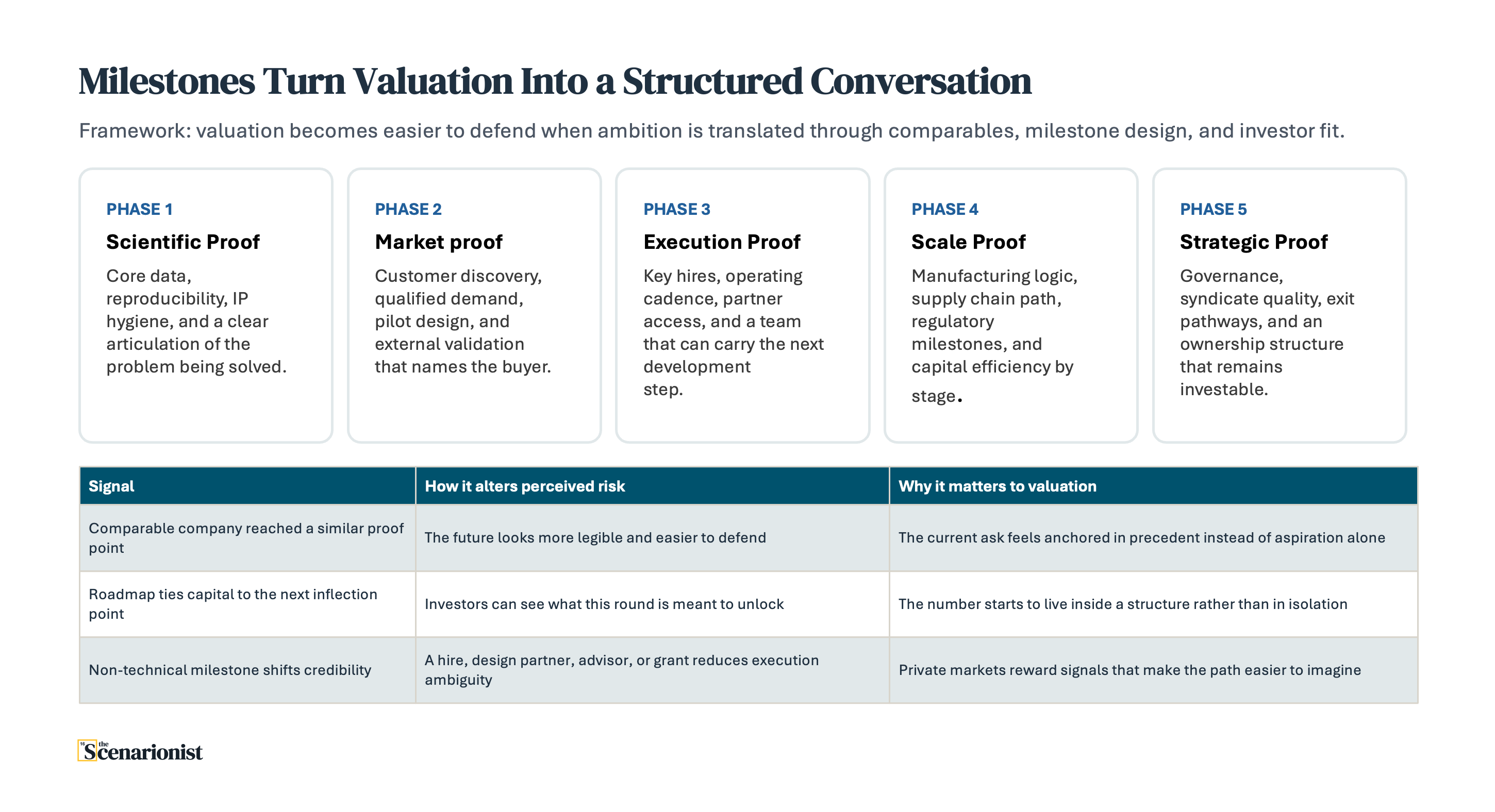

3. Milestones Turn Valuation Into a Structured Conversation

Valuation in deep tech is rarely discovered through a neat formula, because early-stage companies are priced through a conversation about ownership in a future asset whose path remains partially unproven. That conversation becomes more credible when the founder frames valuation through comparables, milestone design, and investor fit, all of which help translate ambition into a structure that can be reasoned about by people who must allocate risk professionally.

Comparables matter because they give investors a precedent for imagination. A founder who can point to companies that moved through similar scientific or industrial gates, and who can explain what happened to valuation after each key proof point was reached, creates a logic of progression that supports the current ask. A roadmap matters for the same reason, because it tells the investor where the company sits today, which milestone increases the next round’s quality, and how the present financing creates a path toward that next increase in value. A thoughtful cap table matters because every share, every option pool decision, and every governance commitment carries a message about the future flexibility of the company.

Optionality deserves equal attention, since founders often understate how much negotiating power comes from a credible ability to pursue grants, strategic partnerships, licensing structures, customer-financed pilots, or a later timing window for capital. Investors read optionality as maturity when it is presented with calm discipline, because it shows that the company is managing time and alternatives with intention. The same principle applies to investor selection, where fund stage, check size, technical familiarity, portfolio engagement, and timeline fit all shape the quality of the partnership that follows the money.

4. The Best Negotiators Design the Room Before They Enter It

Many founders prepare thoroughly for questions and still devote too little attention to the architecture of the conversation, and architecture often shapes the outcome just as much as the answers themselves. The room matters, because the right stakeholders may need to be present at the right time, because allies can create useful momentum before skeptics arrive, and because difficult issues often benefit from careful sequence and from being addressed in stages.

Stakeholder analysis usually sits at the center of this work. It helps to understand who is visible, who holds silent influence, who carries veto power, and which internal incentives may be shaping positions that look purely financial on the surface, because once those interests are mapped with some care, the conversation becomes easier to guide without unnecessary friction. Governance concerns, academic recognition, timing pressure, portfolio optics, and downstream rights can then be addressed with a tone that remains constructive and specific.

Tactical empathy also tends to matter here, and it works best when it is treated as a form of disciplined attention with no need for performance. Labeling concerns, mirroring language, asking calibrated questions, and allowing a little silence can make underlying assumptions more visible, which often improves the quality of the conversation without making the founder sound defensive. Emotional steadiness carries unusual value in deep tech, where the founder’s identity is often closely tied to the science and where the relationship may last far longer than a single round.

BATNA belongs inside the same architecture, because credible alternatives shape confidence even when they are never stated as leverage. Grants, strategic partnerships, a slower timing window, continued technical development, or licensing paths may all influence the conversation indirectly, while investor alternatives often reveal themselves through urgency, sequencing, exclusivity, or internal timing pressure. Once preparation reaches that level, negotiation feels steadier and more deliberate.

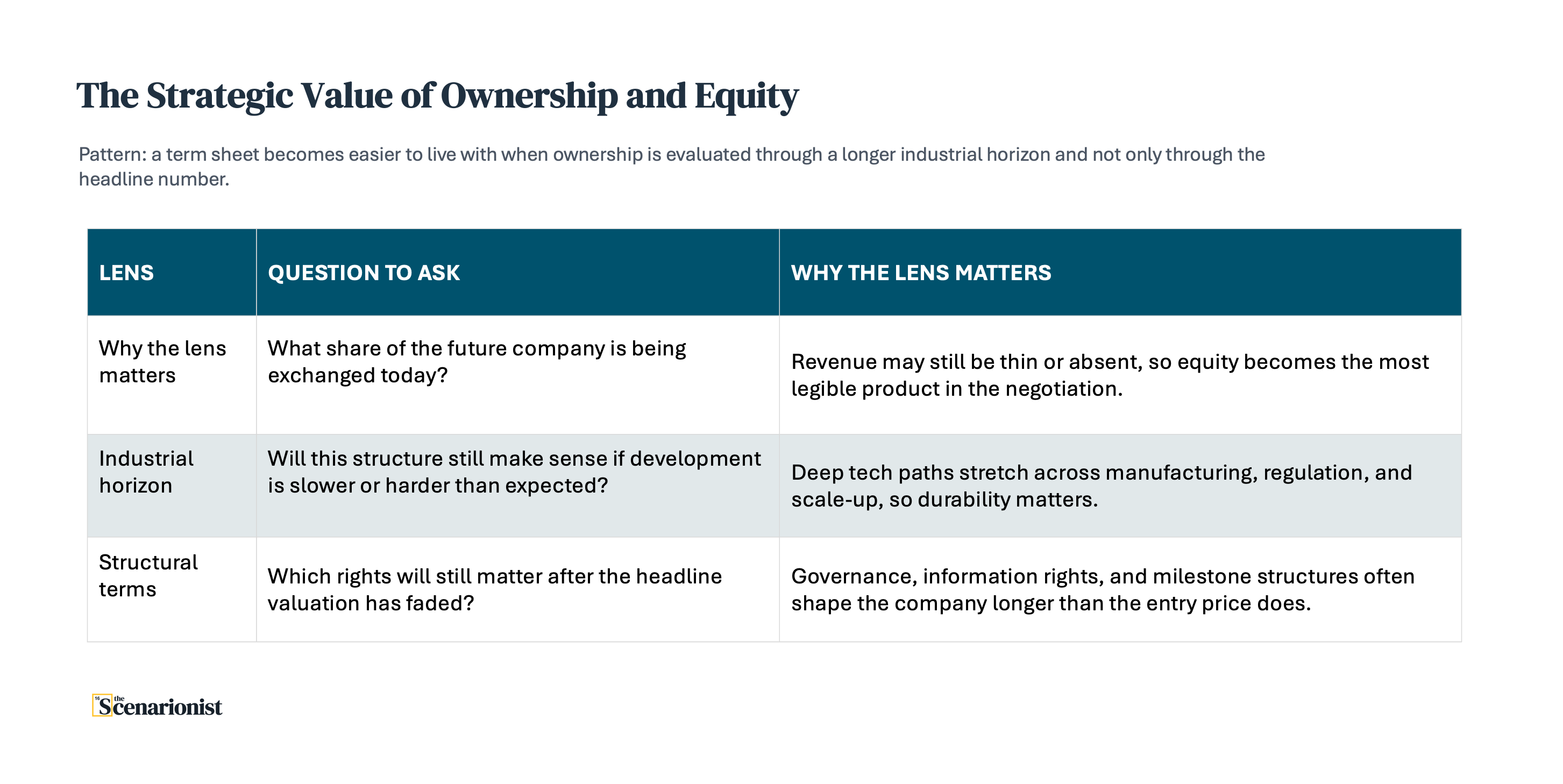

5. The Strategic Value of Ownership and Equity

Investors are funding an invention and purchasing ownership in a company that may eventually turn invention into value, which is why equity carries such unusual importance in early-stage deep tech. Revenue is often thin or absent, and the company’s most legible product becomes a share in a future that still requires interpretation, patience, and proof.

If a term sheet is approached with a longer industrial horizon in mind, the conversation tends to shift toward structural questions that remain meaningful even when the path to market proves slower or harder than expected. Governance, information rights, milestone structures, liquidation logic, and board composition may sit behind the first headline, and they often have more to do with the long-run health of the company than a marginally higher entry valuation.

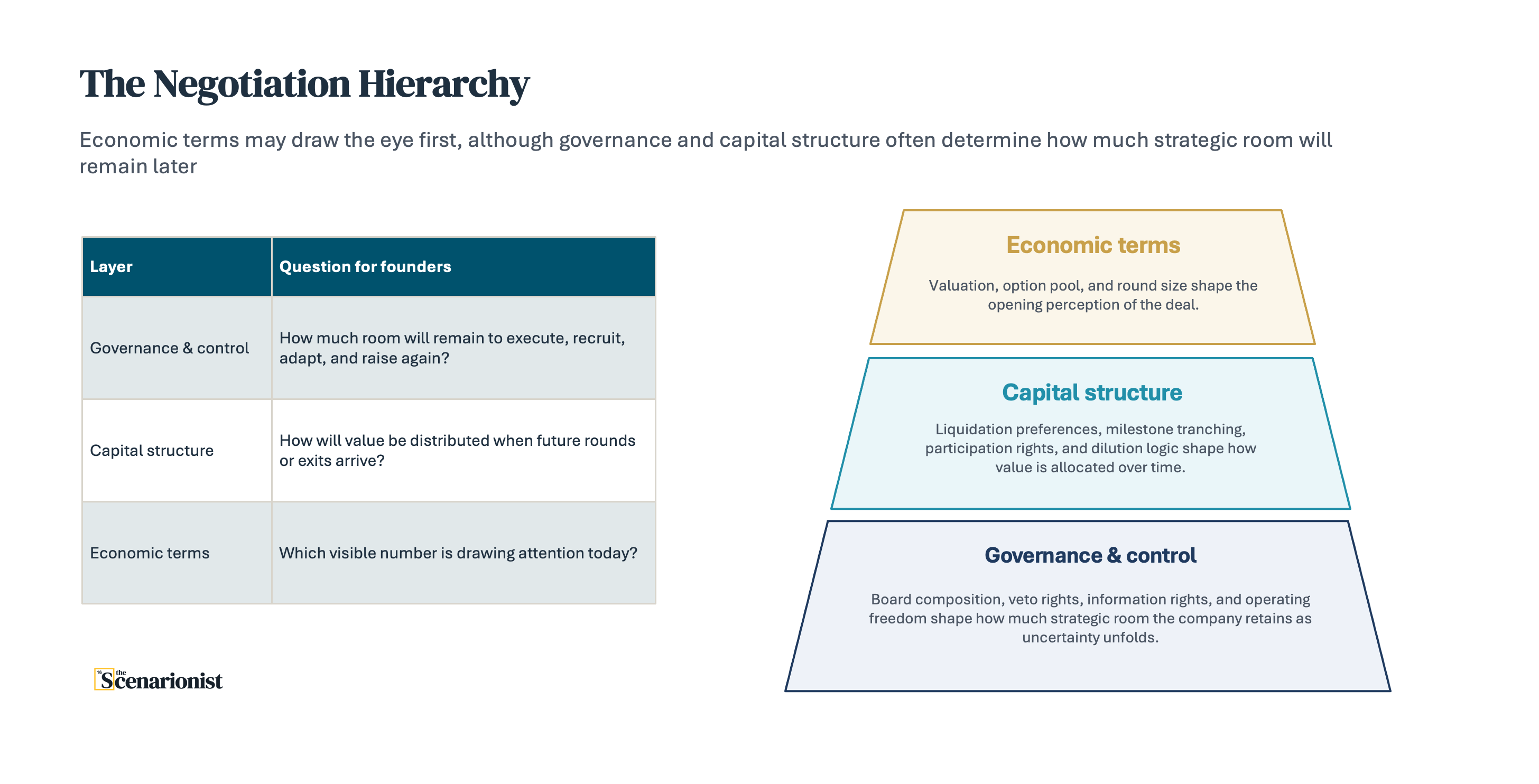

6. Visualizing the Negotiation Hierarchy

A useful visual shorthand is to think of a deep tech deal as a hierarchy, where economic terms attract the most immediate attention, capital structure shapes how value is distributed, and governance determines how much strategic freedom will remain as the company navigates technical and commercial uncertainty.

That hierarchy leaves valuation fully in view. It also suggests that a deal becomes easier to live with when the most visible number is held inside a structure that still leaves the company room to execute, recruit, adapt, and raise again with credibility.

7. Negotiation as Strategic Alignment

In Deep Tech, negotiation often becomes more constructive when it is understood as a process of alignment, because the strongest companies usually gather data, test assumptions, and refine the deal structure until a workable consensus begins to emerge. That scientific posture can be surprisingly effective in the boardroom, where clarity, patience, and intellectual honesty often matter more than rhetorical force.

This wider logic is also the thread that runs through the reading path behind this essay. In Chapter 1, the core negotiation is framed around equity, timing, and the founder–investor gap. In Chapter 2, the focus moves to market, team, and technology as the three pillars of credibility. In Chapter 3, the discussion turns to ownership, valuation, comparables, and investor fit. In Chapter 4, the emphasis shifts toward preparation, stakeholder mapping, sequencing, BATNA, and room design. The Bonus Appendix then adds the tactical layer, where language, calibrated questions, objection handling, and case-based judgment give the framework a more operational form.

READING PATH

The Deep Tech Negotiation Playbook

Chapter 1 — The Deep Tech Negotiation Playbook

Equity, timing, the founder–investor gap, and the opening logic of deep tech negotiation.Chapter 2 — Market, Team, and Technology

The three pillars that turn credibility into leverage before a valuation discussion hardens.

Chapter 3 — Ownership, Valuation, and Investor Fit

Comparables, milestones, ownership design, and the private-market logic of price formation.Chapter 4 — Preparation, BATNA, and Room Design

Stakeholder mapping, sequencing, BATNA, and the architecture of the negotiation itself.

Bonus Appendix — Tactical Empathy and Objection Handling

Language, calibrated questions, tactical empathy, objection handling, and practical cases.

Closing Thought

Deep tech companies rarely arrive at stronger negotiations through urgency or volume. They usually arrive there through clarity that compounds over time, because clarity makes market validation easier to trust, makes team quality easier to evaluate, gives capital planning a visible logic, and allows valuation to rest on something more durable than enthusiasm alone.

Once that foundation exists, the term sheet starts to reflect a relationship between evidence and future value, which is often where a healthier conversation begins. The broader framework naturally extends further, into governance design, milestone tranching, licensing architecture, board composition, investor objections, and tactical language, though even at this stage the central idea remains fairly simple: deep tech negotiation tends to improve when the company makes the future legible without sounding louder than the room requires.

At The Scenarionist, we created The Deep Tech Negotiation Playbook as a dedicated series for exactly this purpose: to help founders, investors, and operators think more clearly about how scientific value becomes negotiating power, and how better structure can support better decisions across the life of a deep tech company.

Let’s keep in touch!

That is all for today. Thank you, as always, for following us every week. ❤️