Inside Deep Tech Exits, Engineered | The Scenarionist

What advanced materials and rare earth recycling exits reveal about underwriting risk, negotiating leverage, and building strategically inevitable companies.

In deep tech, the exit is not a happy accident at the end of a funding story. In advanced materials and rare earth recycling, the exit is often the product. The acquirer is the only customer that matters, and the real work starts years before a banker drafts a teaser.

In deep tech, the exit is not a happy accident at the end of a funding story. In advanced materials and rare earth recycling, the exit is often the product. The acquirer is the only customer that matters, and the real work starts years before a banker drafts a teaser.

The public narrative of venture-backed success still leans on a familiar script. A technology is invented, a market is validated, revenues climb, and at some point a larger company pays a premium to capture growth. That script works well enough for software. It barely describes what is happening in advanced materials, critical minerals, or industrial recycling.

In those sectors, the exit is not an afterthought. It is the central design constraint. A polymer platform, a surface coating, a magnet-recycling process or a rare earth separation technology has little independent destiny. Either it plugs into the value chain of a handful of industrial incumbents, or it remains an impressive pilot that never justifies its capex.

Yet most investment processes still treat exits in these fields as tail events. M&A “comps” are pulled at the back of the deck, a few logos are dropped on a slide, and the assumption is that if the company performs, some strategic will eventually appear. That assumption leaves money on the table. It also misprices risk.

A different approach is possible: treat exits themselves as a dataset, worth mapping with the same discipline applied to mining assay results or wafer yields. Instead of assuming that industrial M&A is noisy and idiosyncratic, treat it as patterned behavior that can be studied, catalogued and used.

The recent waves of exits in advanced materials and rare earth recycling provide enough structure to make that exercise concrete. Deals like the acquisition of a catalytic polymer platform by Danimer Scientific, the acquisition of a surface-coatings specialist by Henkel, and the purchase of a spintronics-based sensing company by Allegro MicroSystems on the materials side, and acquisitions of a UK hydrogen-based magnet recycler by Mkango Resources (through its Maginito subsidiary), an ionic-liquid separation platform by Ionic Rare Earths, and an accelerated solvent-extraction developer by Ucore Rare Metals on the rare earth side, are not random anecdotes.

Together they outline how industrial acquirers think when technology risk, supply chain fragility and policy pressure collide.

When the Exit Is the Product

In software, the exit window opens when metrics signal scalability. In materials and critical minerals, something more structural is at work. The buyer is rarely paying for revenue. The buyer is paying to close a vulnerability.

The chemistry and process platform acquired by Danimer Scientific did not become attractive because it had a sprawling customer base. It became decisive because its catalytic p(3HP) chemistry and process profile slotted into a specific capex bottleneck in Danimer’s PHA build-out.

That acquisition cut future fermentation spending, improved margins and opened an acrylic-acid option. The “product” in that transaction was a shift in unit economics and optionality for Danimer’s platform, not a stand-alone business.

The magnet-recycling company later consolidated by Mkango did not become important because of top-line numbers. It became necessary once hydrogen-based NdFeB magnet recycling aligned with the UK’s national security concerns, EV policy and Mkango’s need to show rare earth execution before its mine reached production. A pre-commercial specialist in magnet scrap suddenly became the bridge between a junior miner’s plans and a government’s industrial strategy.

The accelerated solvent-extraction platform that Ucore acquired did not represent a high-growth operating company in 2020. It represented a separation process that could cut both capex and opex for a domestic refinery that did not yet exist. Ucore was not buying a P&L. It was buying the only credible path it could see to a U.S.-based separation plant with a chance of competing with Chinese incumbents.

In each case, the “product” that cleared the exit was not revenue, but a shift in a system: a lower capex curve, a supply chain hedge, a policy-compliant process. The financial return for investors came from aligning with that system-level value long before it was priced into public markets.

What Exit Mapping Actually Looks Like

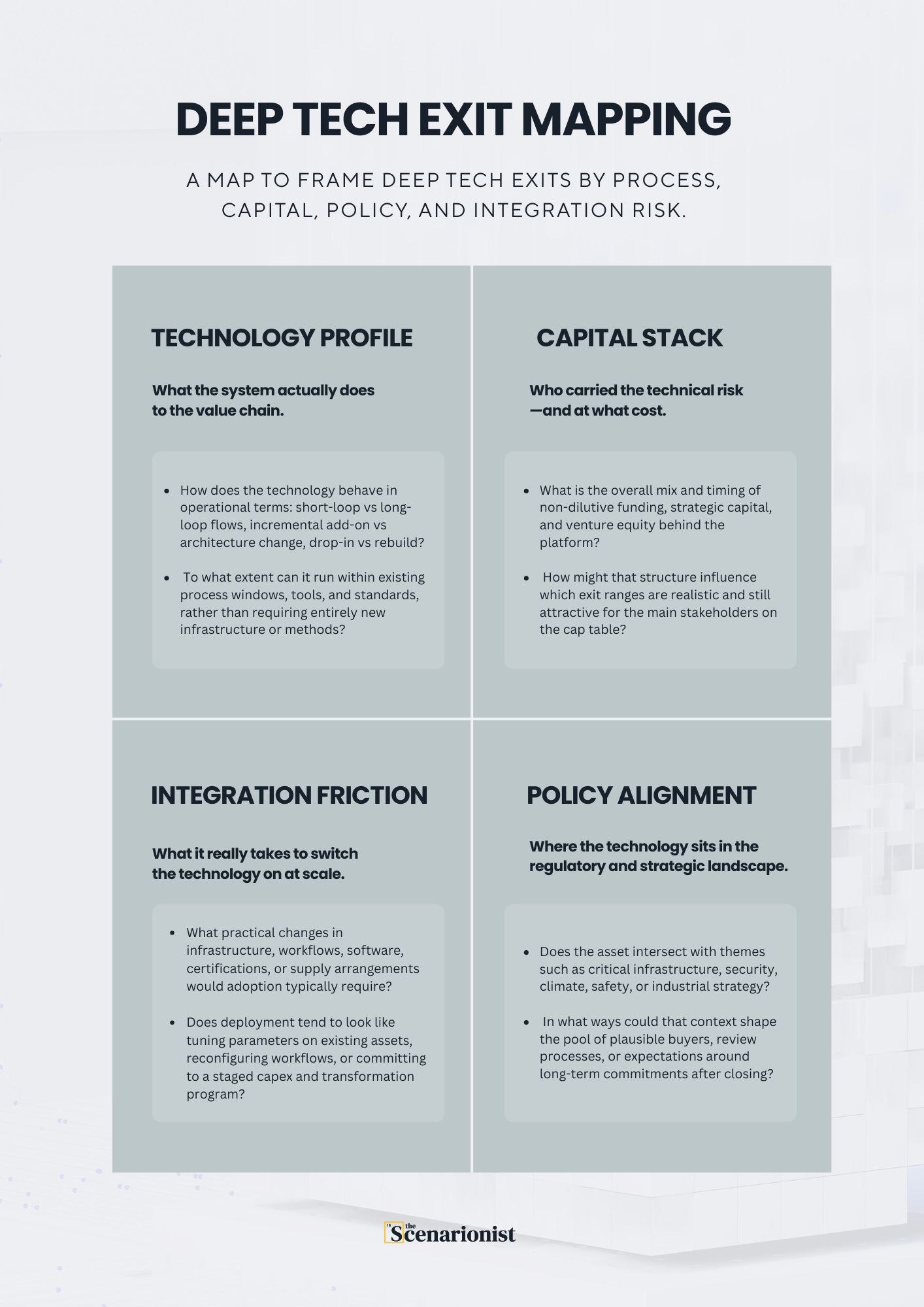

Exit mapping is not a mood board of logos and deal values. A map that deserves the name behaves more like a technical dossier than a pitch deck. For each acquisition, it captures a handful of attributes that industrial acquirers actually care about over cycles.

The first axis is technology profile. Not in marketing terms, but in blunt process language. Is the asset a short-loop process that turns scrap directly into usable alloy, like hydrogen decrepitation of NdFeB magnets? Is it a long-loop chemical pathway that dissolves and separates elements into oxides, using ionic liquids or classical hydrometallurgy? Is it a drop-in coating with curing temperatures aligned with existing lines, or a sensor that can be dropped into legacy PCB footprints without redesign?

These details are not trivia. They determine whether the acquirer must rebuild factories or simply change a line in a work instruction. Most deep-tech pitches gloss over this distinction. Acquirers never do.

The second axis is capital stack. The structure behind the polymer exit into Danimer—heavy use of DOE and NSF grants, a midlife asset sale to a large petrochemical player, and a relatively modest cumulative equity raise—produced a cap table that could accept a mid-nine-figure outcome and still deliver respectable multiples. The magnet recycler acquired by Mkango and the ionic-liquid separation platform acquired by Ionic leaned heavily on UK and EU grants, keeping dilution low and avoiding the pressure for explosive standalone scale. The separation-technology developer later bought by Ucore survived for years on a mix of U.S. Department of Defense funding and small private rounds.

These are not isolated cases. The companies that reached exits in these sectors often treated non-dilutive capital as a core part of their design. That choice preserved flexibility when the strategic window opened. A proper exit map records that behavior.

The third axis is policy alignment. In rare earth recycling and separation in particular, significant transactions rarely occur in a regulatory vacuum. Deals involving platforms later acquired by groups such as Mkango, Ionic or Ucore tend to sit within a broader national-security and industrial-policy context, often subject to additional review or expectations. The specifics vary by jurisdiction, but the pattern is consistent: regulatory posture is not a formality. It influences who is a viable buyer, what long-term commitments are expected after closing, and how far public institutions are prepared to go in supporting deployment.

The fourth axis is integration friction. The coatings specialist that Henkel absorbed invested heavily in ensuring that its products cured at temperatures compatible with existing lines and could be applied with standard equipment. The spintronics-based sensing company designed its TMR sensors so that they could be dropped into PCB footprints originally laid out for Hall-effect devices. The recycled alloy from the UK magnet-recycling process was tested and blended with virgin material without loss in magnet performance.

Each of those decisions turned potential buyers into partners long before a transaction term sheet was drafted. A map that tracks whether a startup has done that work indicates whether the team is building for a trade sale or for a decade of heroic independence.

Once a dataset of exits is structured along those axes, the industrial M&A landscape stops looking like a series of surprises. It begins to resemble a set of routes.

Seeing What the Multiple Hides

Beyond that map, much of the apparent noise in deep tech exits begins to resolve.

Headline deal values in these sectors often look modest. A few million in cash and stock for a separation technology, a mid-eight-figure or low-nine-figure acquisition for a polymer process, a quiet buyout of a coatings platform. On standard venture templates, those outcomes rarely qualify as spectacular.

What the exit map makes visible is the ratio between price and system-level impact. A biopolymer platform that cuts capex on a flagship plant, a fluorine-free coating that sidesteps tightening regulation, or a separation technology that unlocks domestic refining capacity does not sit on the same axis as a typical revenue multiple. The relevant denominator is avoided capex, avoided delay, avoided policy risk.

Once exits are read in that frame, the size of the cheque stops being the main signal. The logic behind the cheque becomes the real object of study.

Advanced Materials and Rare Earth Recycling: Cost, Embeddedness and Security

The advanced materials cluster, taken as a whole, is a study in cost curves and embeddedness. Acquirers in these transactions are not buying “better materials” in the abstract; they are buying targeted improvements to their own production frontier. Catalytic processes that replace part of an expensive fermentation build-out, coatings that meet future regulation without new tools, TMR sensors that drop into existing footprints while upgrading performance—all reduce the friction between current assets and future requirements.

That friction cost explains why embeddedness is a recurring theme. None of the platforms in the advanced materials work require incumbents to rip out lines or reset qualification regimes; matching to curing profiles, equipment and interfaces is already done. From a capital-allocation standpoint, this creates a sharp filter: technologies that demand high-inertia infrastructure changes sit on one side; those that deliver gains through parameter changes rather than plant changes sit on the other. Exit mapping makes clear which side typically gets bought.

The same logic appears in IP: patents are handled less as a static fortress and more as a portfolio of monetizable branches, with some claims sold early to recycle capital and others retained to anchor later corporate acquisitions.

On the rare earth side, the engine is different but equally legible. Here, exits are built at the intersection of security, policy and process economics. Recycling and separation platforms operate at modest physical scale but occupy the point in the chain where policymakers and supply-chain planners feel exposed. That position explains the prominence of grants in their capital stacks and the profile of their acquirers. Junior miners and small listed developers move upstream not for technology risk in isolation, but because owning a recycling or separation platform tightens their narrative around domestic supply.

Public money carries early technical and infrastructure risk; private capital arrives later, on cleaner terms, into a de-risked asset. National-security reviews and defence-linked programs are not side notes; they are part of the design space in which these exits are engineered.

Why This Work Has to Be Done Now

The timing is not incidental. The 2020s are not a calm backdrop for deliberate industrial innovation. Supply chains have become instruments of power. Policy is moving faster than many balance sheets. Regulatory pressure on PFAS, carbon intensity and waste is converging with geopolitical anxiety about China’s dominance in critical materials.

In that environment, the value of disciplined exit mapping is multiplied. Advanced materials and critical minerals are no longer niche curiosity sectors; they are the plumbing for EV adoption targets, grid decarbonization, defense readiness and digital infrastructure. When those systems wobble, the response is rarely a new app. It is an industrial purchase order, a procurement program or an acquisition.

Strategic buyers are already adjusting. Danimer’s move for a catalytic polymer platform, Henkel’s acquisition of a fluorine-free coatings specialist, Allegro’s purchase of a TMR sensor company, Mkango’s consolidation of hydrogen-based magnet recycling, Ionic’s roll-up of ionic-liquid separation and Ucore’s absorption of accelerated solvent-extraction technology all took place in this context. Each transaction drew on years of prior encounters, joint projects and public funding. None of them were last-minute attempts to buy growth. They were structured responses to risk.

Capital markets, by contrast, are still catching up. Many generalist investors continue to evaluate deep-tech deals with mental models built on SaaS. That mismatch leads to mispricing, misplaced expectations and, occasionally, avoidable write-offs. A fund that expects a magnet recycler to behave like a consumer app in terms of growth and financing cadence will be disappointed. A fund that understands in advance how a hydrogen-based magnet recycler or an ionic-liquid separation platform actually exited will set different milestones and negotiate different rights.

There is no shortage of commentary about industrial strategy, “friendshoring” and supply chain resilience. Most of it stays at the level of slogans. The exit maps that matter cut through that noise and show where capital, technology and policy have already met in contracts and closing documents.

Thanks for being here! ❤️

The Scenarionist is not a fan club for deep tech; it is a field manual for the people who have to make it work at term-sheet level. Premium issues go beyond narrative and into the mechanics — who bought what, on which terms, under which constraints, and what that implies for the next cohort of companies. In a cycle where supply chains and policy are moving faster than most decks, that kind of clarity compounds.

That is why the serious side of the table reads The Scenarionist Premium.