How Advanced Materials Exhibit Inverse Correlation in Downturns + Toolkit [Downturn Screening Pack] | The Scenarionist

From risk-off to “real-asset on”: why materials with contracted demand and replaceable value resist drawdowns.

When fear spikes, capital prices collateral. That’s why, in risk-off regimes, sectors tied to atoms — factories, inventories, long-dated contracts — often hold or even gain while story stocks unwind. Advanced materials sit squarely on that side of the ledger. They power aircraft, chips, batteries, and defense programs; they’re qualified, contracted, and hard to replace.

This essay lays out why: from the psychology of flight to quality to the anchoring power of plants, inventories, and multi-year contracts — and when the thesis breaks. It compares three stress periods, shows how VC/PE rotated into hard assets, and closes with operator-level cases and the risk patterns that matter (capex execution, energy sensitivity, export controls).

What you’ll get:

Why inverse beta appears in materials: collateral, contracts, and qualification moats.

Historical stress tests across three drawdowns

Empirical Evidence: Why Assets ‘Fly’ in Fearful Markets.

Capital flows: how VC/PE reweighted to “real assets” in risk-off.

Case studies that surface capex, energy, and export-control risks, across batteries, metals, and magnets

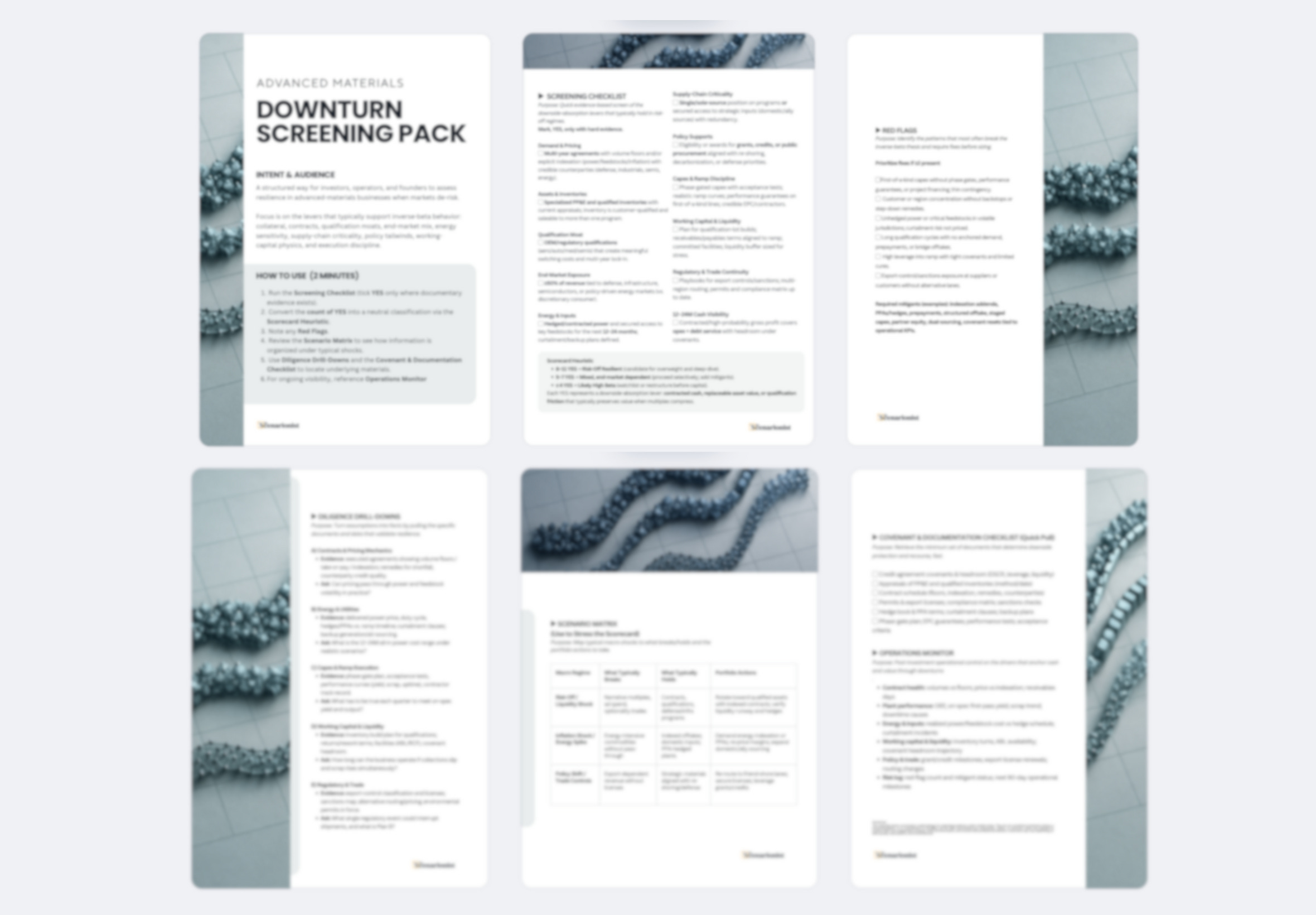

Downloadable Toolkit: Advanced Materials — Downturn Screening Pack

Table of Contents

Introduction: The Paradox of ‘Boring’ Infrastructure and Exciting Markets

“Flight to fundamentals”: why investors seek tangible assets in downturns

Empirical Evidence: Why Assets ‘Fly’ in Fearful Markets

The Venture Capital Flight to Physical Assets

Historical Precedent vs. Contemporary Examples

The Financial Anatomy of Materials Startups During Downturns

The Economics of Materials Startup Resilience

Case Studies

Risks to the “inverse-beta” thesis

Conclusion

Downloadable Toolkit: Advanced Materials — Downturn Screening Pack

1. Introduction: The Paradox of ‘Boring’ Infrastructure and Exciting Markets

Financial history is dominated by intangibles.

In the second half of the 20th century investors glorified software companies whose marginal costs approached zero and whose balance sheets were increasingly dominated by intangible assets. By 2023, intangibles made up over 90% of total S&P 500 assets—a dramatic shift from 1975 when they represented just 17 %.

Many modern firms appear asset‐light because accounting rules do not allow internally generated intellectual property, brands or networks to be capitalized. The result is that markets have come to value growth, network effects and optionality over tangible assets. When valuations depend more on narratives than on replacement cost, investor sentiment swings between exuberance and despair.

However, outside of the limelight of venture‐backed software, a quiet materials revolution is reshaping the physical foundations of the global economy.

Advanced materials such as high‑strength composites, semiconductor substrates, specialty alloys, nanomaterials and novel polymers underpin everything from aircraft and electric vehicles to data centers and quantum chips.

They are the “invisible infrastructure” of modern life; we only notice them when they fail. As infrastructure expert Deb Chachra notes, most people flip a light switch or order a package without ever thinking about the vast network of physical systems behind those simple acts. We expect infrastructure to be boring because that means it is working.

Advanced materials play a similar role: they make our buildings resilient, our airplanes light, our batteries safe and our electronics powerful. Their importance becomes obvious only when supply chains break down or when geopolitical crises reveal critical mineral shortages.

In downturns, when investors flee risky equities and intangible‑rich companies, advanced materials companies often display an inverse correlation with broader market cycles.

2. “Flight to fundamentals”: why investors seek tangible assets in downturns

The refuge of the real

During financial crises investors exhibit a flight to quality, shifting from risky assets (particularly equities) into safer assets such as Treasuries, high‑grade corporate bonds or cash. Investopedia explains that the flight to quality is a “herd‐like movement” triggered by uncertainty; investors may even move into gold despite debates over gold’s industrial usefulness.

Behavioural finance research shows that when fear is high and future cash flows appear uncertain, investors prefer assets with tangible value and stable income streams. This preference extends beyond bonds into commodities, infrastructure and real estate—the so‑called “real asset” classes.

Advanced materials benefit from this psychology because their intrinsic value is tied to physical supply and demand rather than speculative growth.

Materials companies often operate long‑term supply contracts with defence contractors, energy producers or industrial conglomerates. These contracts provide predictable cash flows even when the broader economy contracts. Industry research indicates that defense-sector earnings have low correlation with GDP growth because military procurement depends on geopolitical threats, not consumer sentiment.

During recessions, defence spending often remains stable or even increases as governments prioritize national security. The same is increasingly true for critical minerals and materials used in the energy adaptation; their demand is driven by policy mandates and technological roadmaps rather than consumer whim.

The intangible economy and its fragility

The rise of intangible assets—software, brand equity and data networks—explains much of the volatility in modern market valuations. Nicolas Crouzet and Janice C. Eberly, in a working paper summarized by the UCLA Anderson Review, document that intangible assets now dominate corporate balance sheets.

Sparkline Capital notes that intangible investment surpassed tangible investment around 2000 and constitutes about 40 % of the capital stock. Yet because accounting rules do not capitalize internally generated intangibles, companies heavy on SaaS or brand building, or just aligned with a market sentiment/trend, often appear asset‑light, leading to mispricing.

During bull markets these companies enjoy high valuations because investors project strong growth and network effects. But in downturns, when cash flows become uncertain, the lack of tangible collateral and the difficulty of liquidating intangible assets cause investors to punish them disproportionately.

The intangible economy therefore amplifies market cyclicality.

By contrast, advanced materials companies hold tangible assets—mines, processing plants, reactors, foundries and lab equipment.

They invest heavily in property, plant and equipment, and their valuations anchor on replacement cost, proven reserves and long‑term contracts. When liquidity dries up and intangible valuation metrics (e.g., price‑to‑sales or user growth) collapse, investors often seek companies with hard assets and essential products.

This flight to fundamentals is more pronounced when supply chains are disrupted, as the pandemic illustrated. Meanwhile, intangible‑heavy tech companies may be forced to cut spending on innovation and marketing because their intangible assets cannot be pledged as collateral. The capital intensity and physicality of materials companies thus become protective features in bear markets.